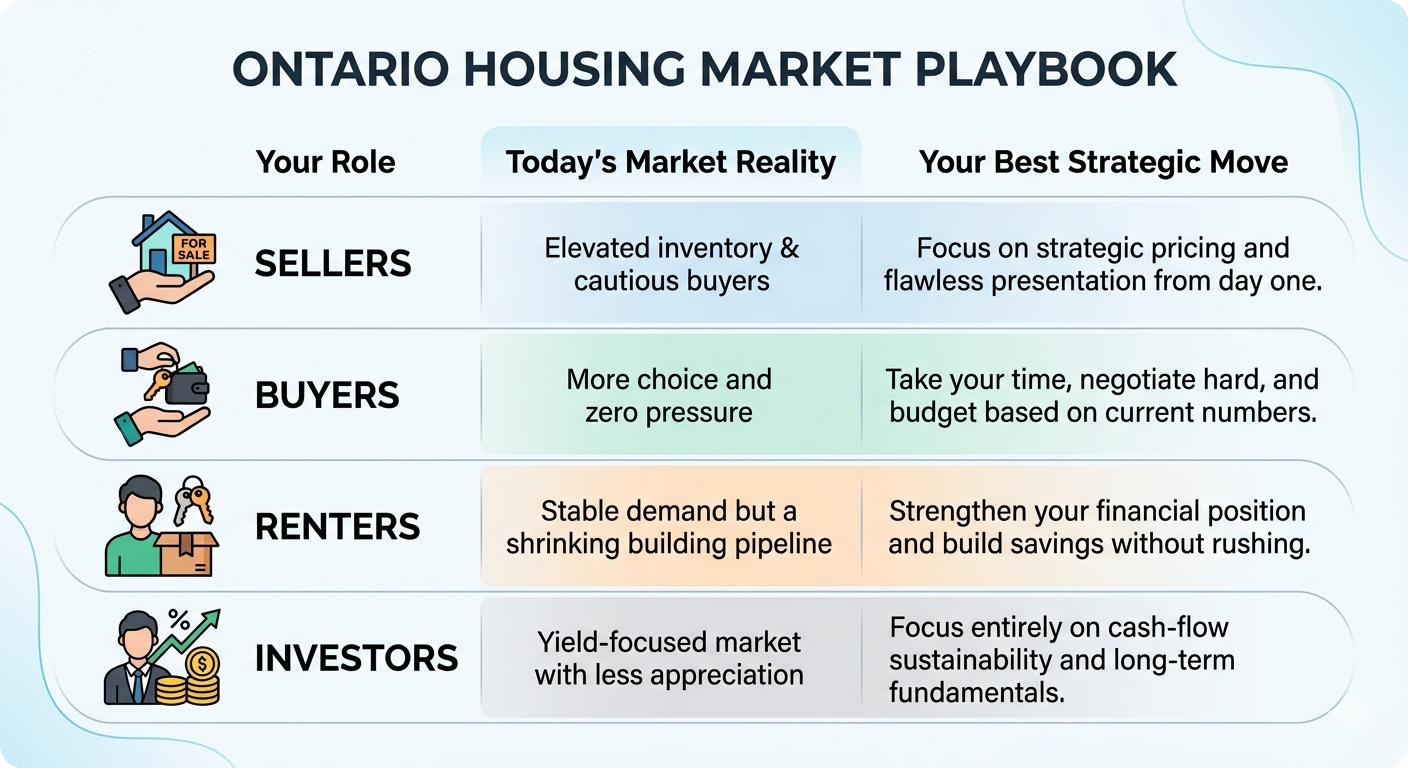

For those following the Greater Toronto Area (GTA) real estate market, the conversation around condos has changed. After a period of intense competition, the market is currently navigating a period of adjustment. Whether you are a first-time investor or simply keeping a pulse on the industry, it is worth looking at the data to understand the current climate.

The Mid-2026 Market Landscape

The Toronto condo market is currently in a phase of stabilization. After the rapid price escalations of previous years, we are now seeing a more balanced environment.

Market Equilibrium: With more inventory available compared to historical lows, the pressure on buyers has eased. This has naturally led to more balanced negotiations regarding price and conditions.

The "Reset" Effect: Prices have experienced a necessary correction from 2022 peaks. For those observing from the sidelines, this provides a clearer picture of value versus speculative pricing.

The Supply Forecast: While there is currently an influx of newly completed units, the pipeline for new project launches has slowed. Given the time it takes to bring new housing to market, this dip in new starts suggests a different supply dynamic could emerge in the latter half of the decade.

Evaluating Pre-Construction in the Current Cycle

Investing in pre-construction requires a different approach than purchasing a resale unit. It is a long-term play that comes with specific considerations.

The Dynamics of Pre-Construction

Deposit Scheduling: Developers typically offer a phased deposit structure. This allows an investor to distribute their capital outlay over several years as the building progresses.

Modernization: New builds often focus on current energy standards and technology integration, which can be an advantage when looking at long-term tenant appeal.

Points of Caution

Valuation Risks: A common concern in a shifting market is the "appraisal gap." This occurs if the market value at the time of completion differs from the initial contract price, requiring the buyer to cover the difference to meet financing requirements.

Timeline Uncertainty: Factors such as labour availability and supply chain constraints can impact completion dates. A realistic timeline is essential when projecting when a unit might be ready for occupancy.

Closing Costs: Beyond the purchase price, it is critical to account for closing costs, including development charges. Transparent contracts that cap these charges provide significantly more predictability for an investor.

Three Perspectives on Condo Investing

For those analyzing the sector, the following three pillars are often at the core of a sustainable investment strategy:

Fundamental Quality: Regardless of the market cycle, the "tried and true" rules apply. Proximity to transit, functional floor plans, and well-maintained building infrastructure are the primary drivers of long-term value.

Due Diligence: The financial health of a condominium corporation is paramount. Reviewing a Status Certificate—which outlines the building's reserve fund, management practices, and any potential legal issues—is the most reliable way to assess an asset.

The Time Horizon: Given the current market transition, the most common strategy for many is a focus on long-term holding. A five-year horizon (or longer) allows an investor to look past short-term volatility and focus on the structural demand for housing in the GTA.

Final Thought

The "best" time to invest is rarely about hitting the absolute bottom of a market; it is about aligning an asset with your personal financial capacity and long-term goals. While the Toronto condo market is currently offering more opportunities than it has in years, it is also a market that rewards patience and careful due diligence. By focusing on the fundamentals—financial health, location, and a long-term outlook—you can move forward with a strategy built on data rather than speculation.

From Loan to Home — Your Trusted Path to Ownership. 🏡