You find the perfect home.

Your offer gets accepted.

Your family starts packing boxes.

Then ten days before closing, you get the call no buyer ever wants:

“Your financing fell through.”

Unfortunately, this situation is becoming far more common in the 2026 GTA real estate market. While the market is stabilizing overall, certain segments—especially condos and pre-construction properties—are seeing failure-to-close rates approaching 30%.

Most buyers are shocked when this happens because they believe they were already approved for the mortgage.

But in many cases, there’s a huge difference between a mortgage pre-approval and a firm mortgage commitment.

The biggest issue?

The person helping you buy the home is usually not the same person responsible for making sure the financing actually works.

That disconnect is where deals begin to fall apart. As someone who is both a Licensed Real Estate Agent and Mortgage Agent, I see this problem all the time. When the real estate strategy and the mortgage strategy aren’t aligned from the beginning, buyers can run into serious issues later in the transaction.

Here are the three biggest reasons deals are failing at closing in today’s market—and how to protect yourself.

1. The Appraisal Gap (The #1 Deal Killer)

As prices adjust in parts of the GTA, some bank appraisals are coming in below the agreed purchase price.

Here’s how it usually plays out.

A buyer agrees to purchase a home for $800,000, but when the lender orders the appraisal, the property is valued at $750,000.

The bank will only finance based on the lower appraised value. That means the buyer suddenly needs to come up with an additional $50,000 in cash to close the deal.

For many buyers, that simply isn’t possible.

Without identifying this risk early, buyers can find themselves scrambling just days before closing—and in some cases, their deposit is at risk.

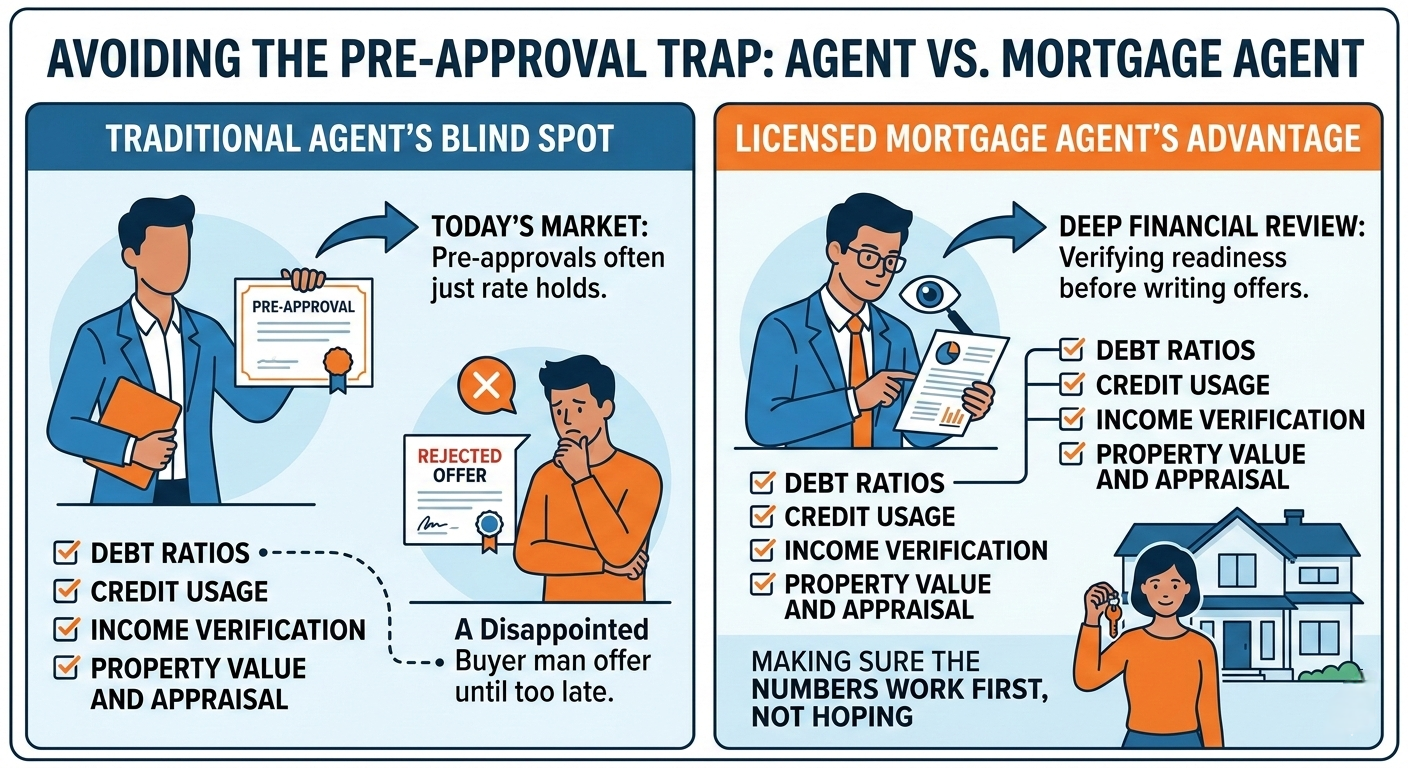

2. The Pre-Approval Trap

Many buyers enter the market with a pre-approval from a bank and assume they’re fully approved.

In reality, many pre-approvals are simply rate holds based on limited information. When the lender eventually reviews the full file, they take a much deeper look at:

• income verification

• debt-to-income ratios

• credit usage

• employment stability

• the property appraisal

This deeper review often happens after the offer has already been accepted. That’s when unexpected problems can appear.

A traditional real estate agent focuses on helping you find the right property and negotiate the purchase. However, they often don’t see the financial details lenders evaluate later in the process.

Because I’m also a mortgage agent, I review the financing side before we even write the offer. I’m looking at your file the same way an underwriter will—so we can identify potential issues early and make sure the numbers actually work.

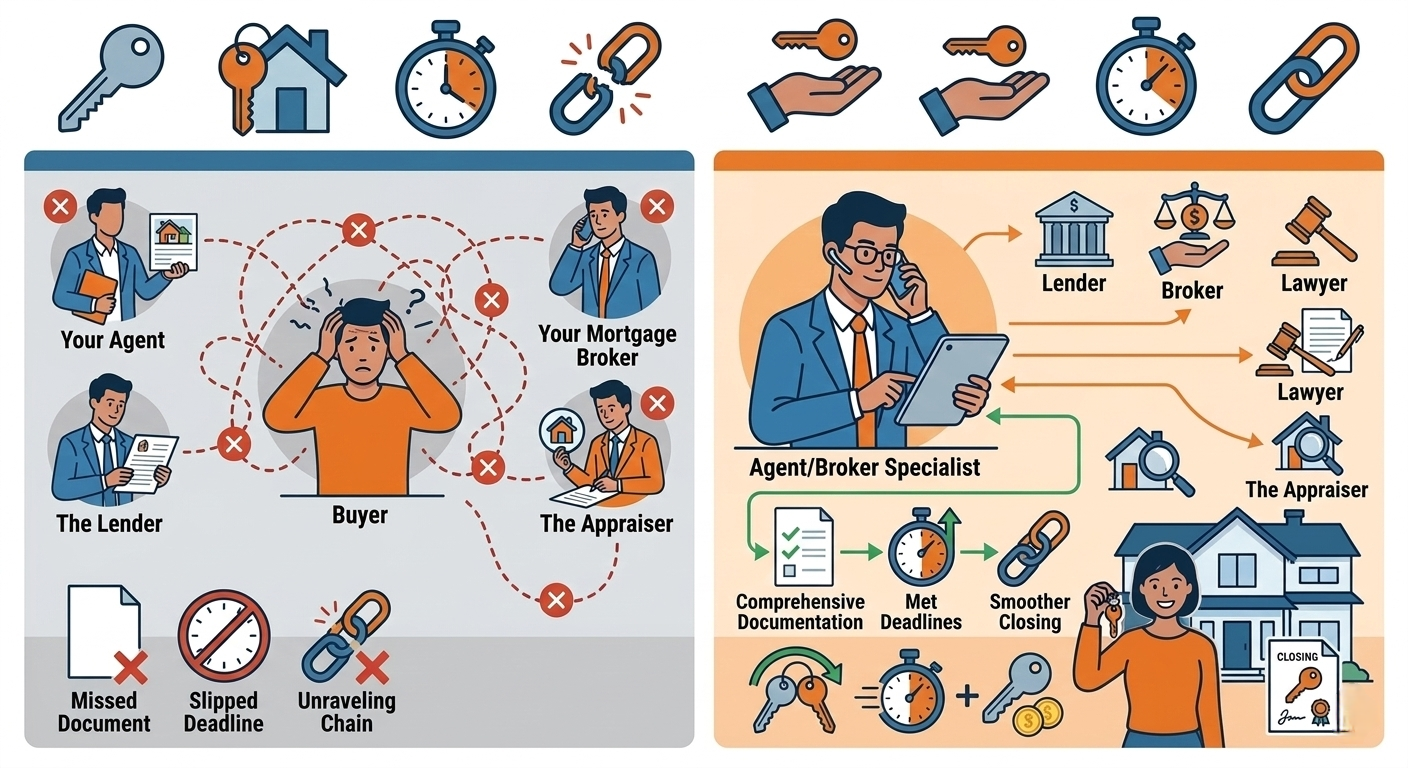

3. The “Game of Telephone”

A typical real estate transaction involves multiple professionals:

• the real estate agent

• the mortgage broker

• the lender

• the lawyer

• the appraiser

When everyone is working on different timelines, communication gaps can happen.

Sometimes deals fall apart simply because of small issues like:

• a missing document

• a delayed appraisal

• a late condo status certificate

• a last-minute lender condition

Suddenly funding is delayed or pulled days before closing.

It’s stressful for buyers and completely avoidable when the process is better coordinated.

How I Help Ensure My Clients Actually Close

As both a Real Estate Sales Representative and Licensed Mortgage Agent, I offer something most buyers don’t get: one coordinated strategy for both the home purchase and the financing.

Here’s what that looks like in practice.

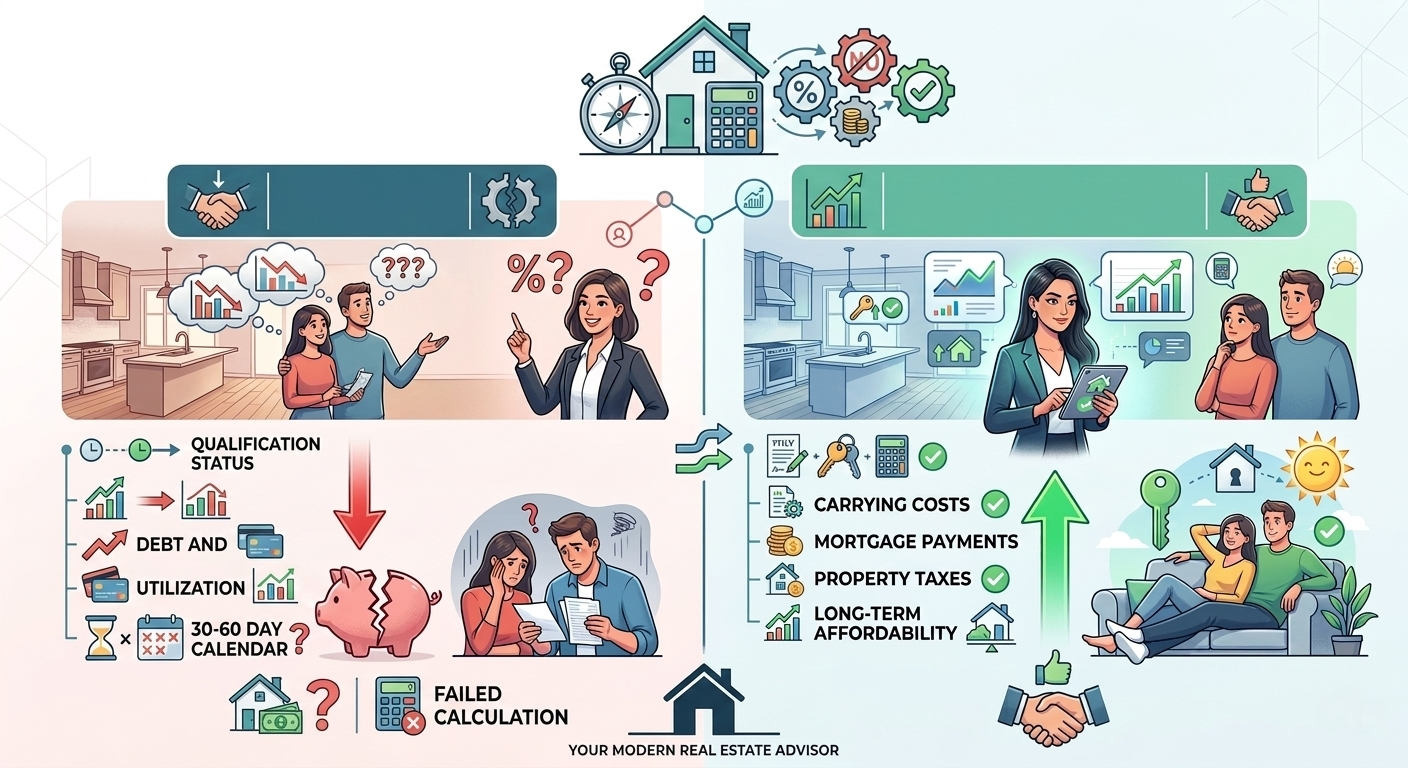

Financial Verification Before We Shop

I don’t just rely on a pre-approval. I review the file to make sure it can actually pass today’s lender guidelines and stress test before we even start looking at homes.

Offers Based on Real Lending Numbers

I guide clients based on what lenders are realistically approving and what properties are likely to appraise for, not just the listing price.

One Coordinated Process

Because I manage both the real estate and mortgage side of the transaction, everything stays aligned from offer to closing.

There are fewer communication gaps, fewer surprises, and a much smoother path to getting the keys.

The 2026 Market Tip Buyers Need to Know

In today’s market, closability matters more than offer price.

Sellers and listing agents are becoming more cautious, and many are prioritizing buyers who can demonstrate strong financing and a solid closing strategy behind their offer.

Having someone who understands both the real estate side and the mortgage side of the transaction can make a major difference.

Because finding the right home is important. But making sure you actually close on it is everything.

Don’t Become a Statistic

The GTA housing market in 2026 leaves very little room for mistakes.

Whether you’re buying a condo, pre-construction property, or detached home, it’s critical to understand both the property side and the financing side of the transaction.

When those two pieces are aligned from the start, the entire process becomes stronger—from the offer you write to the day you pick up the keys.

And at the end of the day, the goal isn’t just getting your offer accepted. It’s making sure you successfully close and walk into your new home with confidence.

From Loan to Home — Your Trusted Path to Ownership. 🏡