In my previous blog, we dug into credit utilization—the “30% rule”—and why it’s one of the most powerful drivers of your credit score. But once that number lands on a lender’s desk, what actually happens can make or break the interest rate you pay. In Canada, this process is called Risk-Based Pricing, and understanding it can save you thousands on your mortgage or loan.

1. What Is Risk-Based Pricing?

Canadian lenders don’t offer a “one-size-fits-all” rate. Your credit score is your risk rating, and it determines your borrowing power:

Tier 1 (760+) – Low risk. You get the lowest rates and strongest negotiating power.

Tier 2 (700–759) – Strong borrower. Competitive rates, but not always the absolute floor.

Tier 3 (650–699) – Fair. Traditional lending applies, but expect a small risk premium.

Below 650 – B-Lending. Higher rates and extra fees to offset lender risk.

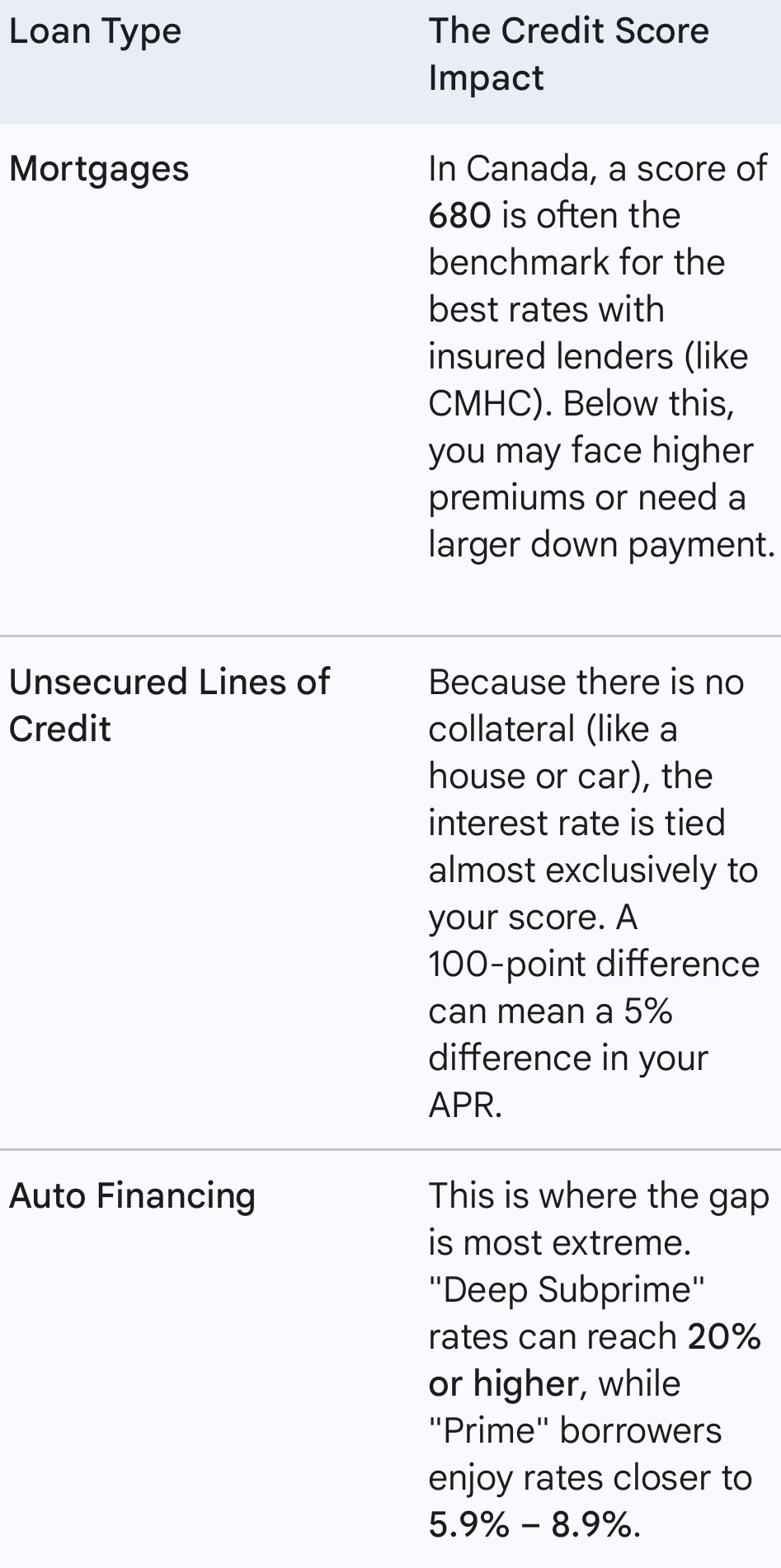

2. How Your Credit Score Impacts Different Loans

3. The “Threshold” Factor

Canadian banks have breakpoints. A score of 720 might get a better rate, while 719 is lumped in with 680.

Pro Tip: If you’re near a threshold, pay down balances before applying—sometimes a 30-day difference can save thousands.

4. Your Score Isn’t the Whole Story

Lenders also weigh:

→ Debt-to-Income Ratio (DTI) – Even a perfect 900 won’t help if your debt exceeds income limits.

→ Public Records – Past bankruptcies or consumer proposals can linger 6–7 years, impacting rates even after your score recovers.

Maximize Your Borrowing Power in Canada

As I’ve mentioned before, understanding credit utilization is just the start. Even a small credit score increase can save tens of thousands in interest. Whether buying a home in the GTA, opening a personal line of credit, or financing a car, your credit score is your strongest negotiating tool.

Next Step: Review your current credit profile and build a plan to move into the next lending tier.

From Loan to Home — Your Trusted Path to Ownership. 🏡