If you’ve been following the GTA real estate market lately, you’ve probably heard a lot about the recent federal mortgage rule changes. The headlines make it sound exciting: more flexibility, easier access to financing, and more options for buyers across Canada. And for many buyers in Ontario—especially first-time homebuyers in the GTA—these updates genuinely can create more opportunities.

But mortgage rules are only helpful when you understand how they actually affect your budget, monthly payments, and long-term financial goals. That’s where I think the real conversation matters.

The Reality Check: Buying a home—whether it’s a condo in Mississauga, a townhouse in Milton, or a detached home in Brampton—isn’t about chasing headlines or reacting to market pressure. It’s about understanding your numbers, knowing your options, and making the right move for your family when the timing makes sense for you.

Here’s a practical breakdown of what these new mortgage changes actually mean in Ontario.

1. The $1.5 Million High-Ratio Insured Mortgage Rule

One of the biggest updates is the expansion of the high-ratio insured mortgage cap to homes priced up to $1.5 million. For buyers in the GTA, that matters.

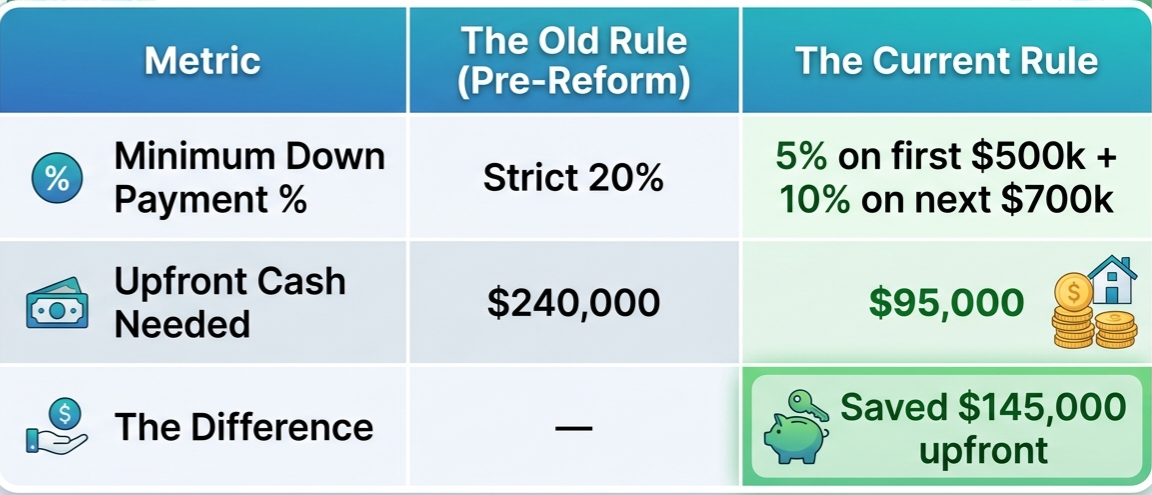

Historically, once a property hit the $1 million mark, buyers needed a minimum 20% down payment. That meant a $1,000,000 home required a $200,000 minimum down payment upfront. For many families in the GTA, especially move-up buyers or younger buyers trying to enter the market, that upfront requirement became the biggest barrier—not the monthly mortgage payment.

Under the updated rules, eligible buyers can now purchase homes priced between $1 million and $1.5 million with an insured mortgage and a lower required down payment.

Example: Down Payment for a $1.2 Million Home in the GTA

The minimum down payment is now calculated on a tiered structure:

5% on the first $500,000

10% on the remaining amount up to $1.5 million

For a $1.2 million home, the shift looks like this:

That’s a difference of $145,000 less upfront. It can significantly change what’s possible for buyers looking at townhomes or detached homes in communities like Brampton, Vaughan, Oakville, Burlington, or parts of Durham.

The Tradeoff: A lower down payment usually means a larger mortgage balance and mortgage insurance premiums added to your financing. It creates flexibility—but it also increases your total borrowing. That’s why it’s worth looking at the full picture before making a move.

2. The 30-Year Amortization Canada Change

The second major update is around the 30-year amortization extension in Canada. Previously, buyers putting less than 20% down on an insured mortgage were generally limited to a 25-year amortization.

Now, eligible buyers can access a 30-year amortization on insured mortgages if:

You’re a first-time homebuyer in the GTA or anywhere in Canada, or

You’re purchasing a newly built construction home

This matters because spreading payments over a longer timeline lowers the required monthly payment. That can improve affordability and may also help with the Canadian mortgage stress test, since lower monthly obligations can support debt ratio calculations.

25-Year vs. 30-Year Mortgage Comparison

(Based on a $600,000 mortgage balance at a hypothetical 4.25% interest rate)

So yes—cash flow improves. But you’re also paying more over time. That’s why this isn’t automatically “better.” It simply gives you another strategy depending on your goals.

Where This Can Help GTA Buyers Most

For many buyers in Ontario right now, inventory remains elevated in several markets and negotiation opportunities are still available. That means these mortgage rule changes can be especially helpful for:

Buyers moving from a condo to a townhouse

Families looking for detached homes in the suburbs

Buyers who have strong household income but haven’t saved a full 20% down payment yet

First-time buyers trying to qualify comfortably while keeping monthly payments manageable

Buyers purchasing pre-construction or brand-new inventory

Used carefully, these rules can create more flexibility. And flexibility can be incredibly valuable in a shifting market.

A Practical Strategy Many Buyers Overlook

One thing I often remind buyers: a 30-year amortization doesn’t mean you’re locked into paying for 30 years. Most lenders still allow prepayment privileges.

That means you can:

Keep the lower required payment now to protect your monthly cash flow.

Increase your monthly payments or make lump-sum contributions later when your budget allows.

This approach gives you the safety net of lower mandatory payments today without giving up the ability to pay the mortgage down faster when household income improves. For a lot of families, that balance matters.

Final Thoughts

The new $1.5M insured mortgage rules and 30-year amortization Canada changes are meaningful. For some buyers, they may create an opportunity to buy sooner. For others, waiting and continuing to build savings may still be the better move. Neither option is automatically right.

The goal isn’t to rush. The goal is clarity.

Understand your budget. Understand the tradeoffs. Understand what ownership looks like beyond the purchase price. And then make your move based on your long-term plan—not market pressure.

Because the best home purchase decisions in the GTA usually happen when strategy leads first.

From Loan to Home — Your Trusted Path to Ownership. 🏡