If you are planning to buy a home in the Greater Toronto Area, renew your mortgage, or improve your financial profile, understanding how credit card limits affect your credit score in Canada is one of the smartest financial moves you can make.

Many Canadians believe that having a high credit card limit is dangerous or encourages overspending. In reality, when managed properly, higher credit limits can actually help improve your credit score.

For buyers preparing to enter the GTA real estate market, this one factor can make a significant difference when lenders evaluate your mortgage approval and borrowing power.

The strategy behind this is called credit utilization.

What Is Credit Utilization and Why It Matters for Your Credit Score

Credit utilization refers to the percentage of your available credit that you are currently using.

In Canada, credit scoring models treat credit utilization as a major factor when calculating your credit score. In fact, it typically accounts for about 30% of your total credit score.

Credit bureaus such as Equifax Canada and TransUnion Canada use this ratio to determine how responsibly you manage credit.

Lenders look closely at this number because it reveals how dependent you are on borrowed money.

For example:

→If your balances are consistently close to your credit limits, lenders may view you as a higher financial risk.

→ If your balances stay low compared to your available credit, it signals responsible credit management.

This is why two individuals with similar incomes can have very different credit scores in Canada.

How Credit Utilization Is Calculated

The formula used to calculate credit utilization is straightforward:

Credit Utilization = (Total Credit Card Balances ÷ Total Credit Limits) × 100

For example:

If you have a credit card with a $10,000 limit and your current balance is $2,000, your credit utilization is 20%.

This percentage is what credit bureaus analyze when evaluating your credit behavior.

Lower utilization generally results in a stronger credit score and a more favorable profile for lenders.

Why Higher Credit Card Limits Can Improve Your Credit Score

It may sound counterintuitive, but having a higher credit limit can actually help strengthen your credit score — as long as your spending does not increase.

Here are two key reasons why.

→ Lower Utilization Automatically Improves Your Ratio

→ Your credit limit is the bottom number in the credit utilization calculation.

When your credit limit increases and your spending remains the same, your utilization percentage automatically drops.

Lower utilization signals to lenders that you manage credit responsibly.

More Financial Breathing Room

Higher credit limits also give you more flexibility for everyday spending without pushing your utilization too high.

For example:

A $2,000 balance on a $5,000 limit equals 40% utilization, which may negatively impact your credit score.

The same $2,000 balance on a $15,000 limit equals 13% utilization, which is far more favorable for credit scoring.

For many buyers preparing for mortgage approval in the Greater Toronto Area, lowering credit utilization is one of the fastest ways to strengthen their financial profile.

3 Smart Strategies to Improve Credit Utilization

If you are planning to apply for a mortgage or major loan in Canada, optimizing your credit utilization can help improve your credit score.

Here are three practical strategies.

1. Keep Your Utilization Below 10%

While many financial experts recommend staying below 30% utilization, borrowers with the highest credit scores typically keep their utilization below 10%.

Lower balances compared to your available credit demonstrate strong financial discipline.

2. Request a Credit Limit Increase

If you have a strong payment history, requesting a credit limit increase can instantly lower your utilization rate.

This works best when you avoid increasing your spending after the limit increase.

3. Pay Your Balance Before the Statement Closing Date

Many people believe credit card balances are reported on the payment due date, but most issuers actually report balances on the statement closing date.

Making a payment a few days before your statement closes ensures a lower balance is reported to the credit bureaus.

This small adjustment can have a noticeable impact on your credit score over time.

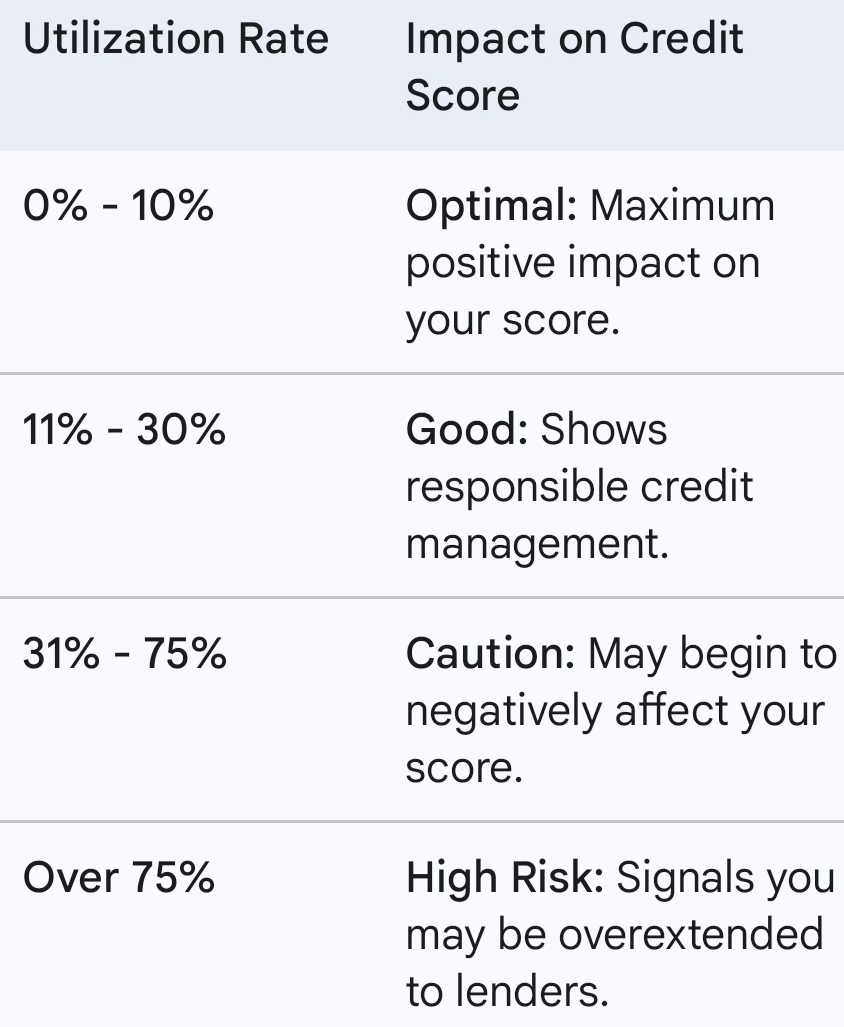

Credit Utilization Ranges and Their Impact on Your Credit Score

Understanding these ranges can help you maintain a strong credit profile.

Why Credit Utilization Matters When Applying for a Mortgage

If you are preparing to buy a home in the Greater Toronto Area, your credit score plays a major role in determining:

→ Mortgage approval eligibility

→ Interest rates offered by lenders

→ Your overall borrowing capacity

Improving your credit utilization before applying for a mortgage can significantly strengthen your financial profile and may help you qualify for better mortgage rates.

For many buyers entering the GTA housing market, this strategy is one of the simplest ways to increase mortgage readiness.

The Bottom Line

Your credit card limit is not just a spending cap — it is an important part of your financial reputation.

By understanding and managing credit utilization, you can strengthen your credit score, demonstrate responsible financial behavior to lenders, and improve your chances of securing favorable mortgage financing.

For anyone planning to buy a home, refinance a mortgage, or improve their credit score in Canada, mastering credit utilization is one of the most effective financial strategies available.

From Loan to Home — Your Trusted Path to Ownership. 🏡