I’ve been in this business long enough to see a pattern most buyers never expect. I’ve seen six-figure entrepreneurs get declined for mortgages. And I’ve seen modest-income earners get approved with zero stress. The difference was never the credit score. It was the paperwork story.

As both your Realtor and Mortgage Agent, my role goes far beyond submitting documents. My job is to make sure your financial story makes sense to a lender the very first time they read it.

Because here’s the truth:

👉 Mortgages don’t fall apart because of bad income. They fall apart because of unclear income. A smooth mortgage approval isn’t luck. It’s clarity, consistency, and strategy.

Why Lenders Care About Your “Story” (Not Just Your Numbers)

Lenders don’t meet you. They don’t know how hard you work. They don’t know your business potential or future growth.

All they see is paper. Your application is reviewed like a file in a courtroom—every number needs context, every gap needs an explanation, and every inconsistency raises questions.

If your documents tell a clean, logical story → approvals move fast.

If they don’t → delays, conditions, or outright declines.

The 3 Biggest “Approval Killers” I See Every Week

These are the most common mistakes that derail otherwise strong buyers—and how we fix them before they become a problem.

1️⃣ The Mystery Deposit

Large or frequent deposits that aren’t clearly explained immediately trigger lender red flags.

Why lenders worry:

Unverified funds could be borrowed money, undisclosed debt, or temporary cash inflows.

The fix:

I make sure every deposit is documented—transfers, bonuses, business income, or gifts. Gifted funds? We prep gift letters and source documents upfront, not last minute.

2️⃣ Credit Spikes Before Closing

New cars. Furniture financing. “Buy now, pay later” plans.

This is one of the fastest ways to kill an approval after you’ve already been pre-approved.

Why lenders worry:

New debt changes your debt-to-income ratios instantly—even days before closing.

The fix:

Simple rule: No new debt until you have the keys.

I walk clients through what not to do so nothing surprises underwriting.

3️⃣ The Income Mismatch

Your paystub says one number. Your T4 says another.

Your tax return says something else. That inconsistency makes lenders nervous—even if you earn more than enough.

Why lenders worry:

They need to understand which income is stable, ongoing, and usable.

The fix:

We proactively prepare a Letter of Explanation that clearly bridges the gap before the lender asks. No guessing. No back-and-forth. No delays.

The “Enough Info” Checklist (Not Overkill, Just Smart Prep)

Over-preparing can confuse a file just as much as under-preparing. Here’s what lenders actually want.

✔️ Employed Borrowers

• Recent paystub

• Employment letter

• T4

• Most recent Notice of Assessment (NOA)

Clean, consistent, and easy to approve.

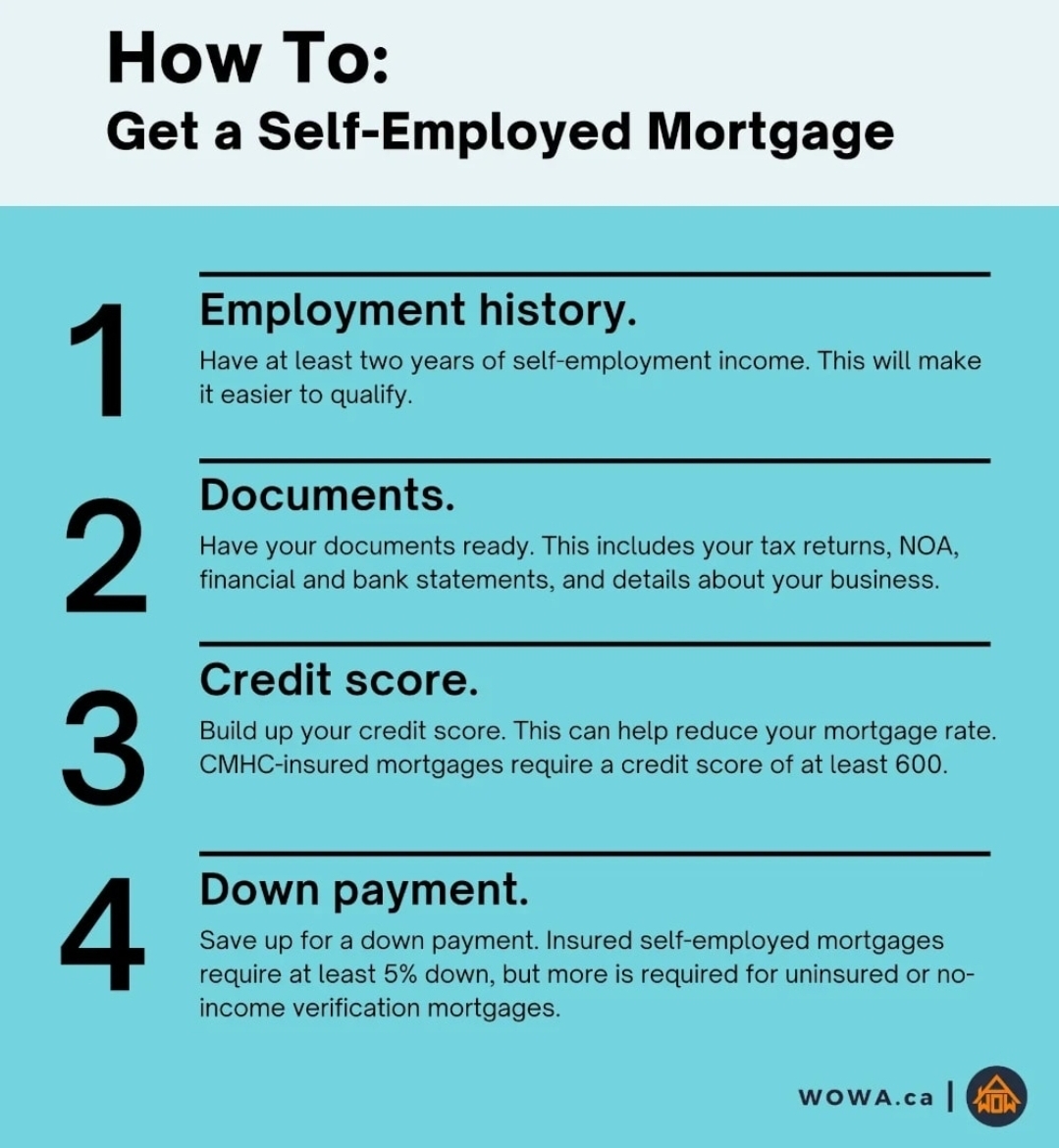

✔️ Self-Employed Borrowers (Where I Truly Specialize)

Self-employed mortgages don’t fail because you work for yourself. They fail because the income story is inconsistent or poorly presented.

What lenders typically need:

• 2 years of Notices of Assessment

• 2 years of T1 Generals

• Business financial context when required

This is where strategy matters most. We position income properly, explain write-offs intelligently, and highlight true earning power—without crossing lender guidelines.

👉 This is the BFS advantage: structuring self-employed files so lenders see strength, not confusion.

Why Having a Realtor and Mortgage Agent Matters

This is where my two hats save clients real stress—and real money.

Because I handle both the financing and the home search, I:

• Bulletproof your mortgage before you write an offer

• Ensure your price range is fully backed by lender logic

• Eliminate last-minute conditions and surprises

• Strengthen your offer in competitive markets

I’ve seen “messy” files turn into success stories—not by changing the borrower, but by organizing the story correctly.

Final Thought: Approval Favours the Prepared

If you’re planning to buy—especially if you’re self-employed, commission-based, or an entrepreneur—your mortgage approval starts months before you shop.

Your income doesn’t need to be perfect.

Your credit doesn’t need to be flawless.

But your story needs to make sense.

And that’s where I come in.

If you’re thinking about buying, refinancing, or just want to know how a lender would view your file today, let’s get ahead of it—before the pressure starts.

Clarity closes deals.

From Loan to Home — Your Trusted Path to Ownership. 🏡