If you've been keeping an eye on the GTA real estate market and wondering whether now is the right time to make a move, the latest May 2026 data from the Toronto Regional Real Estate Board (TRREB) points to a market that is beginning to tighten.

Over the past year, lower borrowing costs, improved affordability, and softer home prices encouraged many buyers to stay on the sidelines. Now, we're starting to see those buyers return to the market and absorb available inventory.

The result? Buyer opportunities still exist, but the window for maximum negotiating power may not stay open for much longer.

What Happened in May 2026?

The biggest story continues to be supply and demand. Home sales increased while the number of new listings coming to market declined significantly.

*Note: If you are tracking historical market charts, TRREB recently updated its historic data to integrate new client boards across the Greater Golden Horseshoe, so you may notice slight adjustments compared to older, static reports.

Looking at the month-to-month trend, the shift becomes even clearer. Seasonally adjusted home sales increased by 10% compared to April, while new listings declined by 2.1%.

In simple terms, more buyers are entering the market while fewer homes are becoming available.

Are Home Prices Starting to Rise Again?

On paper, home prices remain below where they were a year ago. The average GTA home price in May was $1,069,700, down 4.6% year-over-year. The MLS® Home Price Index benchmark was also down 6.7%.

However, year-over-year numbers only tell part of the story.

When we look at month-over-month trends, average selling prices have already started to move upward compared to April. That's often one of the first signs that market conditions are shifting.

If sales continue to outpace new listings through the second half of the year, we could see prices stabilize sooner rather than later, setting the stage for more consistent growth moving forward.

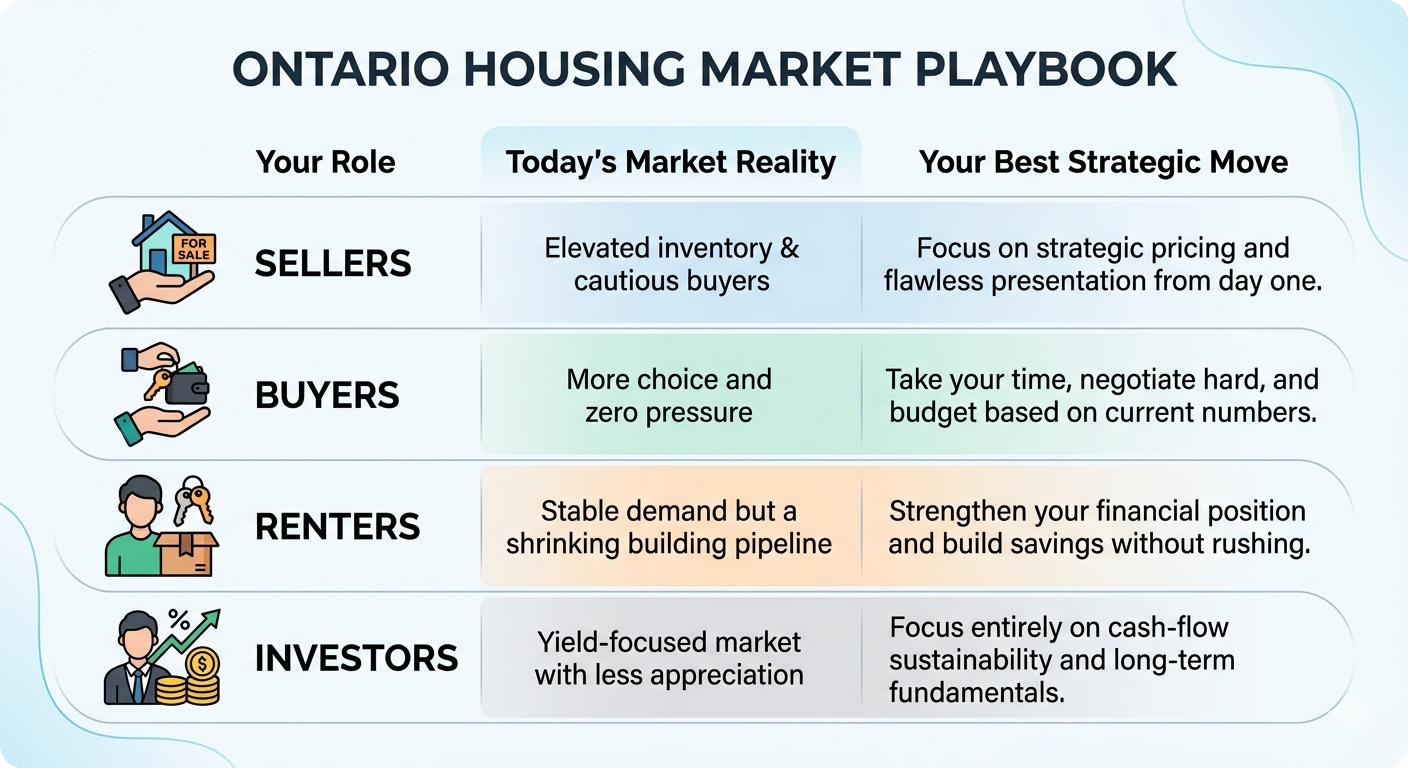

What Does This Mean for Buyers?

Buyers still have opportunities, but conditions are gradually becoming more competitive.

Lower borrowing costs have improved affordability compared to last year, and there are still homes available that offer good value. However, with inventory shrinking, buyers may find themselves facing more competition and fewer opportunities to negotiate aggressively as the year progresses.

Having your financing in place and being ready to act when the right property comes along will be more important than ever.

What Does This Mean for Sellers?

For homeowners considering a move, the current market offers some encouraging signs.

With new listings down nearly 19% compared to last year, there is less competition for buyers' attention. Well-priced homes in desirable neighbourhoods are often attracting strong interest, particularly when they are presented and marketed effectively.

While we're not back to the frenzied conditions of previous years, sellers are beginning to benefit from improving market dynamics.

The Bottom Line

The GTA housing market appears to be moving away from the more balanced conditions we've experienced over the past year.

While buyers still have opportunities, inventory is tightening and market momentum is gradually shifting. As always, real estate is highly local, and what's happening across the GTA may look very different depending on your neighbourhood, property type, and price point.

If you're curious about what these trends mean for your plans, or would like a no-pressure conversation about your home's value or current opportunities in the market, I'd be happy to help you navigate the numbers and create a strategy that works for you.

From Loan to Home — Your Trusted Path to Ownership. 🏡