If you’re thinking about investing in real estate in 2026, you’ve probably asked yourself this:

Should I buy a residential rental property, or is commercial real estate the better move?

With rising costs, tighter mortgage rules, and changing market conditions, this decision matters more than ever.

The truth is—there’s no one-size-fits-all answer. The right strategy depends on your capital, financing ability, risk tolerance, and long-term goals.

As someone who works on both the real estate and mortgage side, I see exactly how deals are structured and approved—so let’s break this down properly.

Residential Real Estate Investing in 2026

Residential real estate continues to be the foundation strategy for most investors.

Why Residential Still Makes Sense

1. Lower Down Payment Requirements

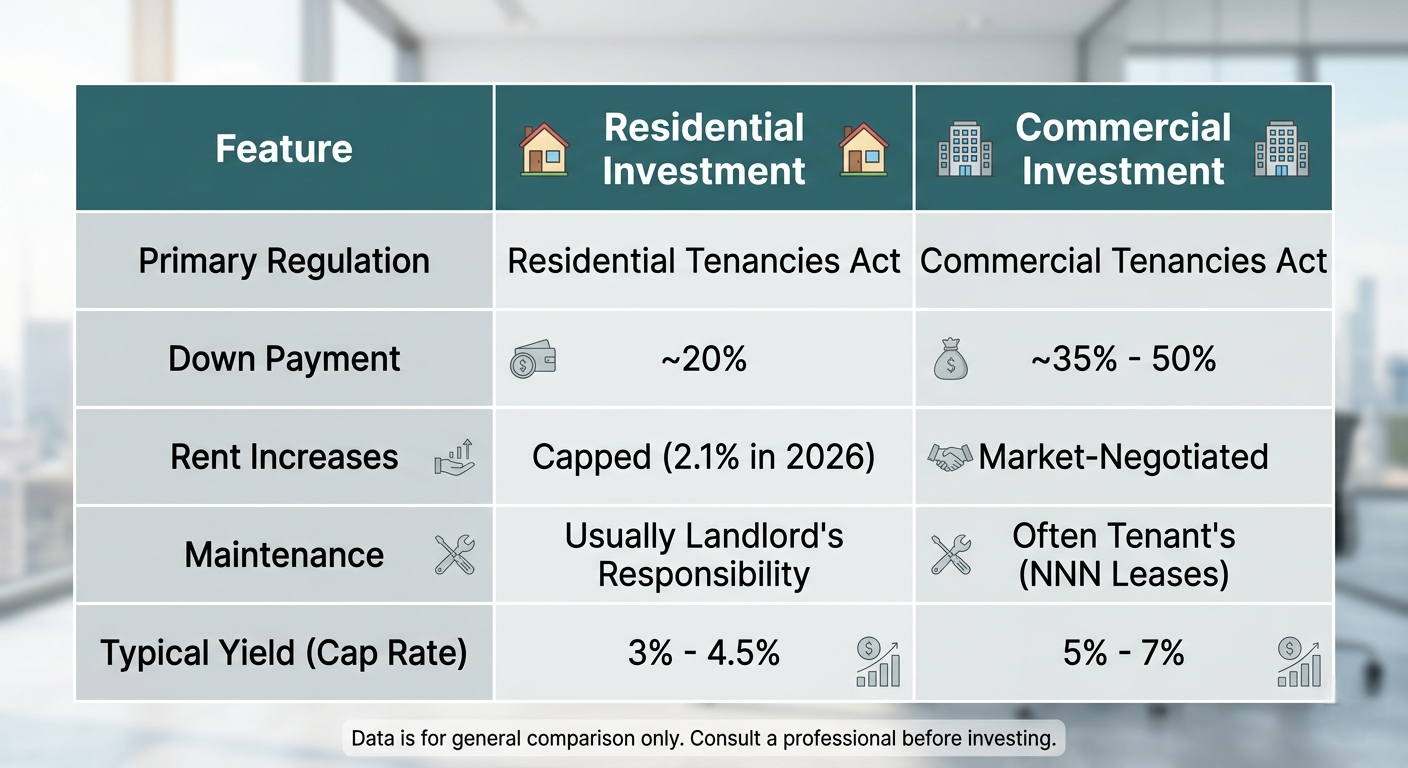

Most residential investment properties require around 20% down, making it the most accessible way to get started or scale.

2. Consistent Rental Demand

Housing will always be in demand. Even in shifting markets:

• Vacancy risk is generally lower

• Tenants are easier to replace

• Demand stays relatively stable

3. Simpler Financing

Residential mortgages are more straightforward. Lenders focus on:

• Your personal income

• A portion of rental income

• Debt service ratios

That said, 2026 lending guidelines are tighter—so structuring your deal properly is key.

4. Better Liquidity

Residential properties are easier to:

• Sell

• Refinance

• Access equity

This flexibility gives you more control long-term.

The Downsides of Residential

1. Rent Control

Ontario’s 2026 rent increase guideline is capped at 2.1%, limiting how quickly you can grow income.

2. Strict Regulations

The Residential Tenancies Act means:

• Evictions can take time

• Non-payment requires legal processes

• Landlords have limited flexibility

3. Cash Flow Pressure

With higher costs and interest rates, many properties are:

• Breaking even

• Or slightly negative monthly

→ Buying the right deal matters more than ever.

Commercial Real Estate Investing in 2026

Commercial real estate is often seen as the next level—but it comes with a very different risk profile.

Why Investors Look at Commercial

1. Higher Income Potential

Commercial properties can generate stronger returns due to:

• Higher rents

• Larger lease values

2. Triple Net Leases (NNN)

One of the biggest advantages in commercial real estate is how expenses are structured. A triple net lease (NNN) means the tenant pays:

• Property taxes

• Maintenance

• Insurance

→ On top of the base rent

So instead of the landlord covering most expenses (like in residential), those costs are passed on to the tenant.

What this means for you:

• Lower out-of-pocket expenses

• More predictable cash flow

• Less hands-on management

You’ll often see this structured as: Base Rent + TMI (Taxes, Maintenance, Insurance)

3. No Rent Control

Commercial leases are fully negotiable:

• No government cap

• Increases based on market conditions

• More flexibility in structuring deals

4. Longer Lease Terms

Leases are often 5–10 years, which can create:

• Stable income

• Less turnover

• More predictability (when occupied)

The Risks You Need to Understand

1. Higher Capital Requirements

Commercial deals typically require:

• 35%–50% down payment

• Strong financials

2. More Complex Financing (Where Most Deals Get Challenging)

Commercial financing is very different from residential—and in 2026, it’s more detailed than ever.

Unlike residential loans, which focus heavily on the investor, commercial lenders focus on the property and its income.

Key factors include:

• Income-Based Lending (DSCR): Lenders calculate the Debt Service Coverage Ratio to ensure the property generates enough cash flow to cover the mortgage. If the property doesn’t “carry itself,” approval may be denied, or you may need a higher down payment.

• Lease Strength Matters: Lenders assess tenant quality, lease length, and lease structure (NNN vs gross). Strong, long-term tenants improve financing options.

• Higher Down Payments & Cash Reserves: Many lenders require 35%–50% down plus reserves to cover vacancies, turnover, and unexpected expenses.

• Detailed Appraisals: Commercial appraisals analyze income potential, lease agreements, market rents, and cap rates—value is based on performance, not just property size.

• Different Rates & Terms: Commercial loans often have higher interest rates, shorter terms (3–10 years), and negotiable structures.

• Vacancy Directly Impacts Approval: Vacancy is a major risk in commercial lending.

• Fully Vacant Properties: Without tenants, lenders may reduce the loan amount, require more down (sometimes 50%+), or decline financing entirely until tenants are secured.

• Partially Vacant Properties: Lenders calculate income based on occupied units and apply a vacancy factor (5–15%). If projected income doesn’t cover the DSCR, they may require higher down, personal guarantees, or reject the loan.

→ Tip: Securing pre-leases or long-term tenants before financing greatly improves approval odds.

3. Vacancy Risk

Even beyond financing, tenant turnover can impact cash flow:

• Vacant units reduce income

• Can take months or longer to replace tenants

• Expenses may still need to be covered in the interim

Residential vs. Commercial: Key Differences

How Rent Collection Differs

Residential

• First and last month’s rent only

• No damage deposits

• Legal process required if tenant stops paying

Commercial

• Deposits are negotiable

• More control through lease terms

• Different enforcement rights depending on the agreement

→ This is a major difference in how risk is managed.

2026 Market Reality

Right now:

• Financing is tighter

• Expenses are higher

• Margins are thinner

That means:

→ You need a clear strategy

→ You need to structure financing properly

→ And the numbers need to make sense from day one

Final Thoughts: What’s the Better Investment in 2026?

If you’re looking for:

• Lower risk

• Easier financing

• A more predictable path

→Residential real estate is still the strongest foundation.

If you have:

• More capital

• Higher risk tolerance

• Experience

→Commercial can offer stronger returns—but it’s not for everyone.

My Approach

I focus on helping my clients build and scale through residential real estate, using smart financing strategies that actually make sense in today’s market.

Because in 2026, it’s not just about buying property—it’s about buying right, structuring it properly, and planning your next move before you even close.

From Loan to Home — Your Trusted Path to Ownership. 🏡